As one ages, there is the possibility that they may incur some sort of physical or mental disability which makes their living at home without home-care services impossible. In such a case, Medicaid planning is an important step to take in order to ensure that you have the coverage that you need and qualify for Medicaid benefits and community-based Medicaid. Medicaid planning well in advance of any disability that affects your ability to live at home is advisable, as there are income limits that must be met in order to qualify for Medicaid benefits and considerations to discuss when making decisions on how to plan your estate in a way that makes receiving Medicaid possible. There are, however, options available to you if you have become recently disabled or are already receiving Medicaid and are worried that your monthly income will exceed the limits set by Medicaid. One of these options is a Pooled Income Trust, which is an irrevocable Special-Needs Trust which allows for disabled and qualified elderly Medicaid participants to place their excess monthly income into a trust run by a non-profit organization. Any income placed into a Pooled Income Trust will not be taken into consideration when determining a participant’s Medicaid eligibility, and the depositor can use the income deposited into the trust to pay for non-discretionary monthly charges and regular bills while still retaining their Medicaid coverage and qualifying for community-based Medicaid services so that they can live in their homes without they need to overburden their family or caregivers. Understanding a Pooled Income Trust and the other Medicaid and estate planning tools available to you will be made easier by the counsel of an experienced Medicaid planning and elder law attorney that will guide your decision-making and ensure that you and your family have the peace of mind in knowing that you will be cared for and able to live in your home and the community.

What is a Pooled Income Trust?

A Pooled Income Trust is a living trust that allows for a disabled or elderly trustee to place their excess income into an irrevocable trust run by a non-profit organization which makes necessary disbursements and payments on behalf of the trustee. Community-based Medicaid services in New York have fixed monthly income and asset eligibility requirements, which for a single individual, aged 65 years or older, is a monthly income of less than $1,677 and liquid assets of less than $30,180. For couples, aged 65 or older, monthly income must be less than $2,268 and liquid assets must be less than $40, 821. Typically, when a participant's income or assets exceed required limits, Medicaid will require them to “spend-down” the excess toward health care costs before they can receive their Medicaid benefits. This often leaves elderly and disabled people in a difficult situation where they cannot afford their health care costs and are ineligible for community-based Medicaid services. A Pooled Income Trust averts this difficulty by placing excess income directly into a Special Needs Trust. The trust, which can have multiple depositors, is run by a non-profit organization specializing in the handling of Special Needs Trusts and allows for the depositor to create an account that pays for non-discretionary recurring charges and monthly bills. Disbursements and payments are handled by the non-profit, or the individual depositor can create a recurring charge that pays automatically for whatever service or bill they need. Alternatively, monthly bills and services can be charged to a credit card and the monthly credit card bill submitted to the trust for payment.

Considerations

There are several considerations to make before creating a Pooled Income Trust. The most important thing to consider is that a Pooled Income Trust is available only for disabled or qualified elderly persons that can prove a disability which hinders their ability to live at home without home-care services. Disability must be proven to Medicaid and any Pooled Income or other Special Needs Trust created must be submitted for approval to Medicaid. A second consideration is that the excess income placed into a Pooled Income Trust cannot be withdrawn as cash. The income that is placed into the trust can only be used for monthly bills and services or other recurring or vital spending. The income can also not be left to accumulate without use, as a Pooled Income Trust does not function the same way as a savings account. The income must be spent and monthly income deposited into the trust in order to ensure maintained community-based Medicaid eligibility. A third consideration is that a Pooled Income Trust is an irrevocable trust, which means that assets and income placed into the trust are impossible to withdraw and the terms of the trust are impossible to change without tremendous difficulty. A final consideration relating to this is that upon the death of a depositor, the income left in the Pooled Income Trust cannot be passed on to a benefactor. Instead, the money must remain in the trust and is then passed on to the non-profit organization to pay any remaining Medicaid liens that remain for the depositor. Any money left over cannot be withdrawn and can then be used by the non-profit for charitable purposes. It is crucial to understand that a Pooled Income Trust does not function as an inheritable asset, but as a practical tool to keep people in their homes and allow them to retain financial independence.

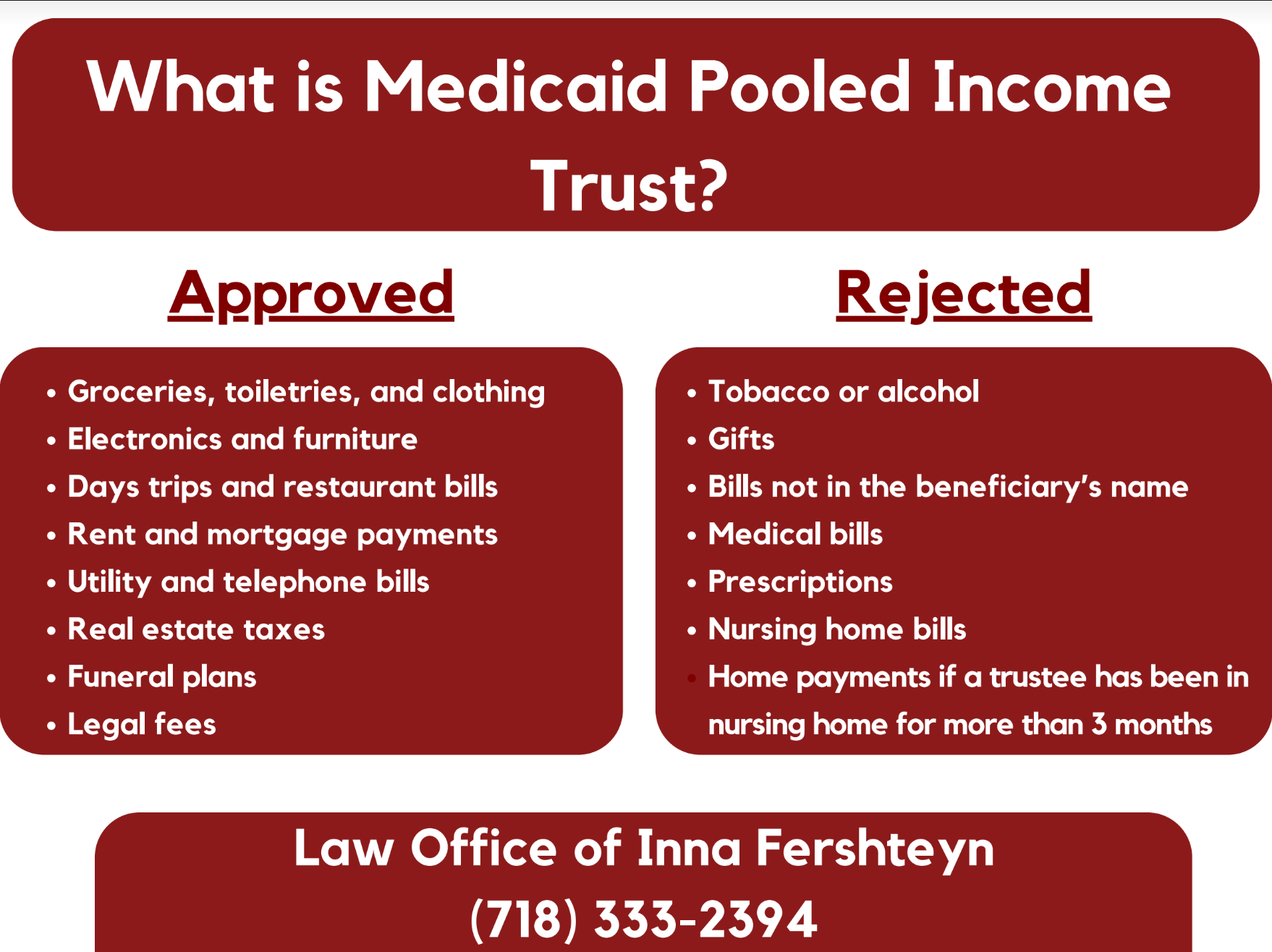

What can a Pooled Income Trust pay for?

A pooled income trust can pay for:

- Groceries, toiletries, and clothing needed by the trustee,

- Electronics and furniture purchased for the trustee,

- Days trips and restaurant bills,

- Rent and mortgage payments,

- Utility bills,

- Real estate taxes,

- Telephone bills,

- Funeral plans,

- Legal fees.

This is certainly not an exhaustive list but some examples of the non-discretionary and recurring charges that those who create a Pooled Income Trust can use their excess income to pay for. Trustees are advised to use their income to make such payments monthly so that excess income does not accumulate.

What cannot be paid for with a Pooled Income Trust?

A Pooled Income Trust cannot pay for:

- Tobacco or alcohol,

- Gifts,

- Bills not in the beneficiary’s name,

- Medical bills,

- Prescriptions,

- Nursing home bills,

- Rent or mortgage payments if a trustee has been living in a nursing home for longer than three months,

- Purchases not made for the beneficiary.

Conclusion

There are options available to disabled and otherwise eligible elderly Medicaid participants to retain their eligibility for home-care services and remain in their homes if they have excess income over Medicaid required eligibility limits. One such option is the Pooled Income Trust, and in order to understand better what such a trust entails and the other estate and Medicaid planning options available to you, engaging the counsel of an experienced Medicaid planning and elder law attorney will help tremendously. To schedule a consultation, call the Law Office of Inna Fershteyn at (718) 333-2394.