Medicaid Planning and Eligibility in New York

Medicaid planning is a sophisticated aspect of estate planning that can help you become eligible for Medicaid assistance. In the long run, Medicaid can help you save money even if your income and assets are currently too high to qualify. The process of Medicaid planning in New York is complex, as the application process can be time-consuming and regulations may change frequently. To comply with Medicaid rules, it is crucial to begin planning early, ideally at least 5 years before needing long-term care. This is due to the Medicaid “look-back” period, which examines your financial transactions over the past 60 months to ensure you have not transferred assets for less than fair market value to qualify for Medicaid.

Whether you are planning early or need immediate assistance, it is highly recommended to consult with an experienced and qualified Medicaid planning attorney in New York who specializes in elder law. An expert attorney can help navigate the intricacies of Medicaid regulations and ensure that your loved one can receive the necessary care without exhausting your assets.

What is Medicaid?

Medicaid is a state-administered health care coverage program funded jointly by state and federal governments. Each state operates its own system, leading to variations in coverage and eligibility across the country. Medicaid is designed to assist individuals with little to no income, and eligibility is determined based on various factors such as pregnancy, age, disabilities, and more. Although Medicaid covers about one-fifth of Americans, a significant portion of its spending is directed towards the elderly, with individuals aged 65 and older receiving the most benefits.

In New York, Medicaid participants have access to a wide range of health care providers, often with no costs aside for copayments. New York Medicaid is divided into two main programs: New York State Nursing Home Medicaid and New York State Home and Community Based Medicaid. Under these, there are additional categories such as Regular Medicaid and Medicaid for the Aged/Blind/Disabled. Each program offers different services, has distinct eligibility requirements, and has varying look- back periods.

To understand the differences between these programs and determine which one is right for you, please carefully review this page. A Medicaid planning lawyer in New York City can help clarify these complexities and ensure you obtain the Medicaid coverage you need in New York.

To schedule a medicaid planning and medicaid asset protection consultation, call the Law Office of Inna Fershteyn at (718) 333-2394 or use the ‘SCHEDULE CONSULTATION’ button below.

New York Medicaid Eligibility Requirements

To be eligible for New York Medicaid, you have to be a resident of New York State, a U.S. national, citizen, permanent resident, or legal alien, in need of health care/insurance assistance, whose financial situation would be characterized as low income or very low income. You must also be one of the following:

- Pregnant, or

- Be responsible for a child 18 years of age or younger, or

- Immigration status, or

- Blind, or

- Have a disability or a family member in your household with a disability, or

- Be 65 years of age or older.

What is Medicaid Planning?

Medicaid planning involves assisting a potential Medicaid applicant in preparing for and submitting their Medicaid application. This assistance can range from simple tasks, like collecting and preparing necessary documents, to more complex activities, such as restructuring finances to meet eligibility requirements. Medicaid planning becomes particularly intricate when an individual’s monthly income or assets exceed the eligibility requirements.

To protect your assets and qualify for Medicaid, it’s crucial to engage in Medicaid planning with an experienced Medicaid planning attorney in New York City. Medicaid rules allow for a look-back period of up to five years, during which any asset transfers can be scrutinized to ensure they were not made to qualify for benefits. Therefore, early planning is essential to avoid penalties and ensure eligibility.

The consequences of being investigated and denied by Medicaid can be severe, impacting both financial security and health. This underscores the importance of consulting with a qualified elder law attorney who can navigate the complexities of Medicaid planning.

At the Law Office of Inna Fershteyn, we assist clients in thoroughly structuring their financial resources. This can involve relocating assets, preparing documentation, and setting up trusts and estates to maximize the likelihood of being accepted into the Medicaid program. Our goal is to safeguard your assets while ensuring you meet Medicaid eligibility requirements.

For individuals and families looking to secure their financial future and access necessary healthcare, Medicaid planning offers a strategic approach to navigating the often complex Medicaid system. Engaging in this process early and with expert guidance can provide peace of mind and financial stability.

New York Medicaid Application Process

While applying for Medicaid can initially seem daunting, having a clear understanding of what it entails can significantly ease up the process. It is important to keep in mind that different eligibility groups will have different application requirements.

You may be eligible to apply for Medicaid in New York if you are a New York resident, U.S. citizen, permanent resident, U.S. national, or a legal alien. Furthermore, you must meet one of the following criteria: be pregnant, have a child(ren) under the age of 18, be certified as blind, or have a disability (or have a family member who is). You must also fall within the low-income bracket.

There are four different ways an individual can apply for Medicaid:

- Applying through NY State of Health: The Official Health Plan Marketplace

- Applying through a Managed Care Organization (MCO)

- Calling the Medicaid Helpline at (800) 541-2831

- Applying through your Local Department of Social Services Office

Where you apply for Medicaid depends on your eligibility group. In New York, your eligibility group is determined through Modified Adjusted Gross Income (MAGI) rules, which primarily considers income and household size.

- For adults 19-64 years of age who are not eligible for Medicare, pregnant individuals, or parents/caretakers:

- Apply through NY State of Health.

- For adults over 65 years of age, or individuals certified blind or disabled:

- Apply through your Local Department of Social Services Office or a Facilitated Enroller for the Aged, Blind, and Disabled.

Following this, you must gather the necessary documents for your application. Here are some

-

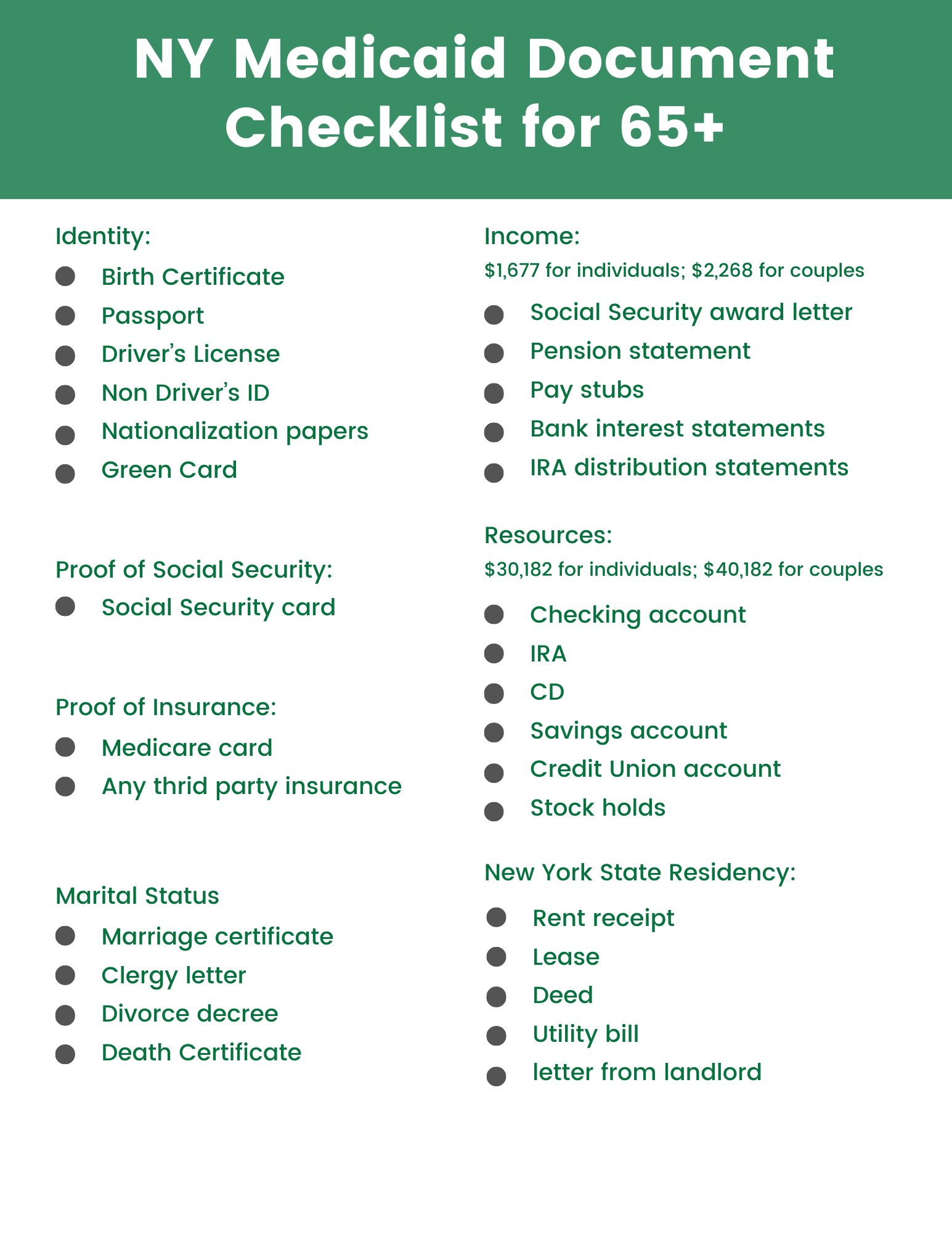

- Proof of Identity and Citizenship: certain documents (like a U.S. passport or driver’s license) can verify both requirements at once. Other forms of verification require supplementary documents to fulfill both (for example, a birth certificate can only be used to prove your citizenship, but not your identity). It is suggested that you go through the list of all the applicable documents to see what you need.

- Home Address Verification: the proof must be dated within the last six months of the application. Some apt documents include utility bills, property tax records, letters from landlords, and more.

- Income Verification: applicants must prove all sources of their income. This includes wages, self-employment, unemployment benefits, child support, and more. You need one proof for each type of income you have, and the proof must be for the last four weeks.

Keep in mind that additional documents may be needed if you have recently lost coverage, are currently insured, or are pregnant.

Once you submit your application, the state will review your submission. It can take up to 90 days to determine your eligibility.

How a Medicaid Planning Lawyer in New York City Can Help

As applying for Medicaid is often a complex and time-consuming process, it is important that you seek guidance from a qualified Medicaid planning lawyer in NYC that can help bypass any hurdles you may encounter.

One of the biggest challenges applicants face when trying to sign up for Medicaid is navigating the numerous eligibility requirements. The complex array of documents and criteria required by each state can make it difficult for individuals to keep track of their application, especially given the lengthy process. Fluctuations in your income can also impact your eligibility and make it difficult for an individual to be properly enrolled in the correct Medicaid program. Incomplete or incorrect applications can then derail your application’s chance of being accepted.

Another prominent issue deals with the complexity of the process itself—whether it be due to the technical jargon, lack of clarity, or highly specialized procedures, many individuals find it difficult to understand exactly what is needed by the state and how to execute these steps in an efficient manner. Uncertainty regarding the wait time can further make it seem as if your application is in flux and can place excess stress on the applicant.

One additional challenge may emerge following the submission of your application: the risk of denial. In New York, it can take up to 90 days for your application to be reviewed, and if your application is denied, you must work as quickly as you can to rectify its shortcomings. There are three different routes you can choose: one can either request a reversal of the decision, re-apply for Medicaid, or appeal the denial. The step you choose to take is largely contingent on your individual situation; consequently, it is recommended that you get in contact with a New York Medicaid Attorney that can help you figure out the best plan for you and your family.

A New York Medicaid planning attorney can significantly reduce these burdens and ensure that your application is both prompt and accurate. At the Law Office of Inna Fershteyn & Associates, P.C., individualized consultations can help you prepare the documents you need, determine your eligibility, and clear up any lingering confusion about the process and how Medicaid can be useful for you and your family. All services are available in both English and Russian.

Why Choose The Law Office of Inna Fershteyn

Having spent many years working in Big Law, Ms. Fershteyn soon realized that her true passion lay in the face-to-face interactions afforded by smaller, more personalized firms. As a result, when she established the Law Office of Inna Fershteyn & Associates, P.C., where she serves as principal New York Medicaid attorney, her goal was to build strong, lasting bonds with clients—driven by a desire for meaningful human connection, rather than by the mere pursuit of wealth. She has upheld this commitment to the individuals she serves for the past 27 years.

While many legal appointments can feel impersonal and transactional, every consultation at the Law Office of Inna Fershteyn & Associates, P.C. is conducted with the client’s best interests at heart, whether that be through personalized solutions, a prioritization of client comfort, or genuine care for each individual involved. Ms. Fershteyn’s thorough understanding of New York law has allowed her to craft nuanced, tailored solutions for over ten thousand clients. It is with this expertise and her proactive nature that she has been able to become a staple in her Brooklyn community, as well as land herself a place on the prestigious 2025 New York Metro Super Lawyers list.

Ms. Fershteyn regularly maintains contact with her clients even after services are complete and aims to create long-lasting relationships that go beyond typical business interactions. She welcomes all clients with open arms and is always eager to support you and your family in any way she can.

If you require any assistance, please do not hesitate to contact the Law Office of Inna Fershteyn at (718) 333–2394 or use the ‘SCHEDULE CONSULTATION’ button below.

New York Long-Term Care Medicaid Requirements

What is Medicaid Long-Term Care?

Long-term care enables patients, usually either disabled or elderly, to get assistance with the many “activities of daily living”. This includes chores such as cooking, cleaning, and getting ready for appointments as well as medical care. The goal of long-term care is to allow patients access to their desired lifestyle when they may be unable to do so themselves. New York City long-term care providers provide alternatives to nursing homes for patients who wish to remain in the comfort of their homes by providing personalized care. With the four options available, it’s important to plan for the possibility of long-term care.

New York Medicaid Long-Term Care Eligibility

- Income Eligibility: For a single individual, aged 65 years or older, monthly income must be less than $1,800. For two people, aged 65 or older, monthly income must be less than $2,433.

- Asset Requirements: A single applicant, aged 65 or older, can have less than $32,396 in liquid (countable) assets to be eligible for New York Community (home care aid) Medicaid. A couple, with both applicants aged 65 or older, can have less than $43,781 in liquid (countable) assets to be eligible for New York Community (home care aid) Medicaid.

- First, determine if your asset is a countable asset or an exempt asset. Homes, home furnishings, and vehicles are considered exempt.

- Second, all the assets of a married couple, regardless of whose name the asset is in, are considered jointly owned and are counted towards the asset limit.

Look-Back Period: The look-back period for an applicant applying for long-term care Medicaid in New York is 60 months. All gifts and asset transfer in the 60 months prior to the date of application are subject to review and Medicaid eligibility requirements.

New York State Nursing Home Medicaid Eligibility Requirements

Who does this cover?

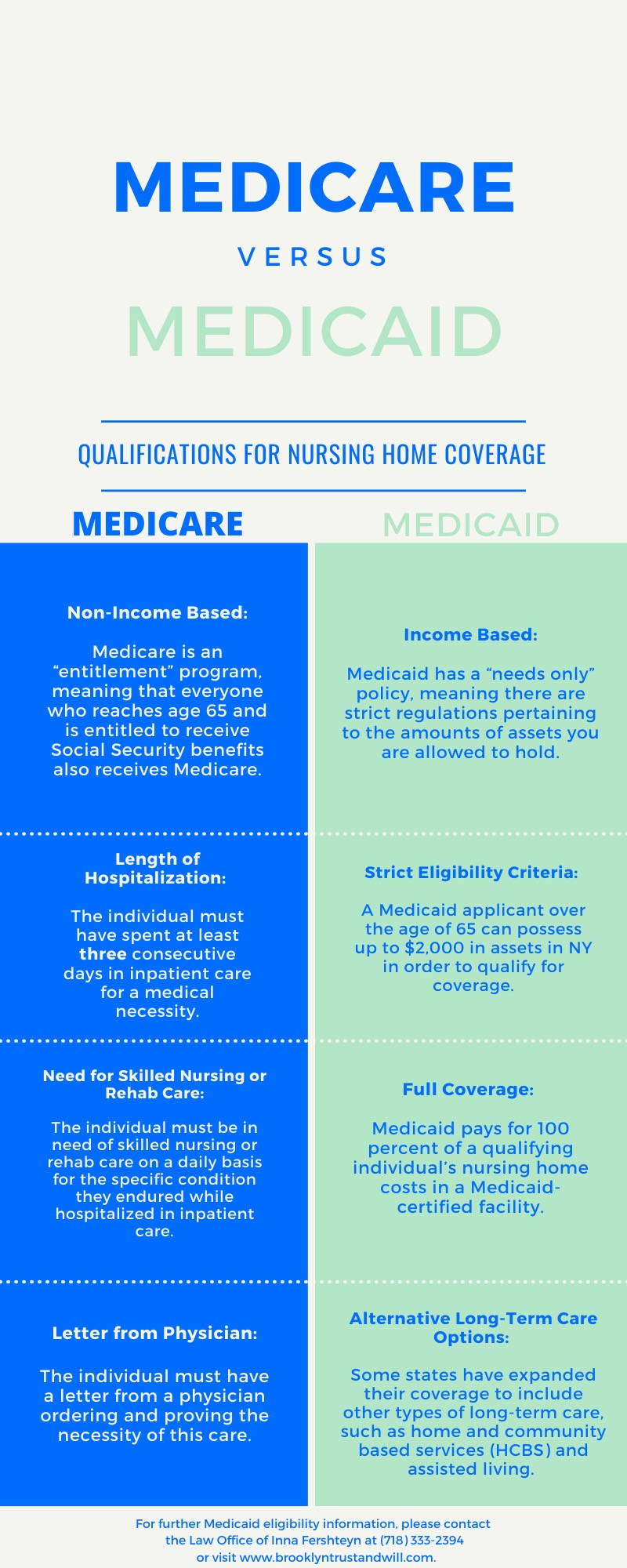

Nursing Home Medicaid in New York provides coverage for individuals needing long term nursing home care. This coverage is primarily aimed at seniors and individuals with disabilities who require a higher level of care than can be provided at home or in an assisted living facility.

What is required to qualify?

- Must be a resident of New York State

- Must be a U.S. national, citizen, permanent resident, or legal alien.

- Monthly income allowance is $50. All other income must be used towards nursing home care.

- Resources must not exceed $30,182

- Home equity must be within $1,071,000 with intent to return

Types of Long-Term Care Facilities in New York

- Nursing Homes- Nursing homes are one of the most popular types of long-term care. They provide 24-hour nursing care to individuals who are chronically ill or injured, have health cliare needs and personal needs, and are unable to function independently. However, a nursing home goes beyond medical care. It’s a place where patients can go on with their lives – and even engage in many activities they may have never taken part in before – while under the secure and capable watch of a team of trained caregivers.

- Residential Homes for the Aged- These facilities only provide residents with room and board and some assistance with personal needs such as eating and grooming. However, homes for the aged are neither staffed nor licensed to provide nursing care. Instead, they are designed to provide a place for people who are able to care for themselves with little or no help. Someone who lives in one of these facilities has to be physically and mentally capable of finding their way to safety in the event of an emergency without assistance from someone else.

- Assisted Care Living Facilities- Assisted living is a middle ground between homes for the aged and nursing homes. Assisted living is a long-term care option for seniors who need more assistance than is available in a retirement home, but who do not require the intensive medical and nursing care provided by a nursing home. Many seniors relocate to an assisted care living facility after rehabilitating in a nursing home or hospital, while others come directly from their homes. These facilities provide the same services as a home for the aged and assistance with medications. Some facilities are even staffed and licensed to provide care for people who have some memory loss or are in the early stages of Alzheimer’s.

- Home Health Care- Home health care agencies provide skilled nursing and rehabilitative care, such as physical, occupational and speech therapy. Personal services, like help with bathing and grooming, are also available. If a physician determines that an individual is in need of home health care, services complementing the physician’s recommendation (ex: help with house cleaning or grocery shopping) are also available.

Can I transfer my assets to children just before I go into a nursing home and qualify for Medicaid?

No, transferring your assets right before going into a nursing home will make you ineligible for Medicaid for the next 5 years. This is because long-term care Medicaid has a five-year look-back period, under which individuals who have made or received any asset transfers must wait until five years after the transaction to apply for Medicaid or face a penalty if they apply prior. When transferring your assets, you need to keep in mind that once you make a transfer, it cannot be reversed. A Medicaid planning attorney will better help you understand the Medicaid lookback period and whether you qualify for Medicaid coverage.

What are the best Nursing Home Medicaid Planning Strategies in NY?

- Spend Down Assets- One way to reach or stay below the Medicaid asset limit is by spending down assets. There are several ways to do so. For example, home modifications and improvements, such as adding a chair lift, purchasing medical devices that are uncovered by insurance, like wheelchairs, and paying off one’s mortgage or credit card debt. It is important to note that one may not give away assets or sell them for under market value because this may result in a period of Medicaid ineligibility. This is known as the Medicaid look-back rule, which is a period of 5 years before the date of one’s Medicaid application where all past asset transfers are reviewed.

- Medicaid Asset Protection Trust- A Medicaid Asset Protection Trust (MAPT) is a particular type of exempt trust used to deposit an individual’s surplus income or assets and therefore preserve their monthly excess income. Medicaid can disregard the deposited money. By depositing the surplus, an individual can lower their total income which is counted by Medicaid, and be within the allowable income limit. Although there is no limit as to the value of the assets that can be placed in this type of trust, MAPTs are a violation of Medicaid’s look-back period. Violating the look back period could result in a penalty period of Medicaid ineligibility, therefore these trusts should only be used well in advance of the need for long-term care Medicaid. If Medicaid is needed in the near future, this strategy is not suggested.

- Spousal Transfers & Refusal- According to current Medicaid laws, transfers may occur between spouses without being subject to the five year look-back period. The assets who are under the name of the spouse in need of care should be transferred to the name of the spouse who doesn't require care, typically referred to as the community spouse. With the presence of spousal refusal, the community spouse may refuse to provide necessary support to the spouse in need of care. If this is the case, then the spouse who is in need of care will immediately be provided Medicaid services to ensure that they are provided with all necessary care. Spousal refusal is present in New York, however it may not be present in other states.

New York State Home and Community Based Medicaid

Who does this cover?

New York State’s Home and Community Based Medicaid covers individuals in the aged, blind, and disabled category. This includes:

- Individuals aged 65 and above

- Individuals certified as blind by the Commission for the Blind and Visually handicapped.

- Individuals certified as disabled by Social Security or New York State

What is required to qualify?

- Residency in New York State

- U.S. citizenship or satisfactory immigration status

- Medical necessity demonstrated through a need for community-based long-term care services

- Income must not exceed $1677 per month for an individual and $2268 per month for a couple

- Resources must not exceed $30,182 for an individual and $40,821 for a couple

BREAKING NEWS: New York Community Medicaid Changes for 2025

In 2025, certain OTC drugs products (including nasal products containing oxymetazoline and glucose tablets) will no longer be reimbursable under Medicaid. Furthermore, newly proposed federal cuts to healthcare programs may result in reduced services and coverage for individuals across the state.

The laws and procedures surrounding Medicaid are constantly changing. If you're an individual who is currently receiving benefits or is in the process of applying for Medicaid, it's important to stay updated on these changes to make sure you don't jeopardize losing your benefits.

How to Apply for Medicaid in New York?

To apply for Medicaid in New York, you have several options:

- NY State of Health: The Official Health Plan Marketplace

- A Managed Care Organization (MCO)

- The Medicaid Helpline- (800) 541-2831

- Your Local Department of Social Services Office

Medicaid eligibility in New York is determined using Modified Adjusted Gross Income (MAGI) rules. Here's how you can apply based on eligibility groups:

- For adults aged 19-64 not eligible for Medicare (MAGI Eligibility):

- Apply through NY State of Health.

- For adults over 65, blind, or disabled (Non-MAGI Eligibility):

- Apply through your Local Department of Social Services or a Facilitated Enroller for the Aged, Blind, and Disabled.

These options ensure you can apply for Medicaid based on your specific eligibility criteria in New York State.

In order to qualify for New York Community Medicaid (Home Care Aid), the following documents are needed:

New York Medicaid: Commonly Asked Questions

What is the difference between Medicaid and Medicare?

Medicaid is a state and federally funded program that provides health coverage for low-income individuals who are eligible. Medicare, on the other hand, is a federal health insurance program for people 65 and older. It also covers individuals who are under 65 with certain disabilities.

Do I need Medicaid if I have Medicare or private insurance?

Even if you already have Medicare or private insurance, you may still need Medicaid. That’s because Medicare and most private health plans typically do not cover long term care services such as home attendants or nursing home stays. Medicaid is often the only program that pays for these essential services. If you qualify, Medicaid can help reduce or eliminate out of pocket costs for long term care that other insurance plans don’t cover.

Can I keep any of my income if my spouse needs Medicaid?

Yes, if your spouse needs Medicaid, you are allowed to keep a portion of income, known as the Minimum Monthly Maintenance Needs Allowance (MMMNA). If your income exceeds this MMMNA, you may be required to contribute 25% of the excess income toward the cost of your spouse’s care at the institution.

How can a trust help in Medicaid planning?

A trust can help protect your assets and ensure Medicaid eligibility. By placing assets into an irrevocable trust, they are no longer considered part of your estate for Medicaid purposes. This can help you meet Medicaid’s asset limits while preserving your wealth. It is essential to hire an attorney, like Inna Fershteyn, to set up your trust correctly and comply with Medicaid’s rules.

What is a 'penalty period'? Do penalty periods apply to all Medicaid applications?

A penalty period is a length of time during which Medicaid will not pay for long term care services because the applicant gave away or transferred assets for less than fair market value within the look-back period, which is generally five years. Penalty periods only apply to Medicaid applications for long-term care, such as nursing home or home care benefits. They do not apply to standard Medicaid applications for general health coverage. The duration of the penalty depends on the total value of the transfers and the average monthly cost of care in your state.

Can I transfer assets to qualify for Medicaid in New York?

Yes, but you have to be careful. Medicaid has a look-back period, typically five years, during which they review any asset transfers. If you transfer assets during this period, you may be subject to a penalty that delays your eligibility for Medicaid. It is a good idea to consult with an attorney who deals with Medicaid, like Inna Fershteyn, to understand the rules and avoid penalties.

Can I get reimbursed for bills I paid before applying for Medicaid?

Yes, you may be reimbursed for bills paid before applying for Medicaid, as long as they were for services received either on or after the first day of the third month before your application month. You can also be reimbursed for bills paid until you receive your Medicaid card. After applying, reimbursement depends on whether the provider accepts Medicaid.

What is the income eligibility limit for New York Home Care Aid Medicaid in 2024?

Individual income level limits for 2024 are $1,677 monthly/$20,121 yearly. Income level limits for couples are $2,268 monthly/$27,214 yearly.

How does New York Medicaid verify income?

New York State’s Medicaid Program has access to an applicant’s IRS and Social Security information. They can tell if the applicant underreported their income and will open an investigation if necessary.

What assets are exempt from Medicaid lien by New York Medicaid?

Assets exempt from Medicaid in New York include an applicant’s primary residence, household items and appliances, personal effects, one motor vehicle that must be used for transport, a burial plot, burial fund up to $1,500, term life insurance, and, in some cases, 401(k)/IRA retirement accounts. A Medicaid planning attorney will help to determine exactly which of your assets will be exempt from Medicaid eligibility considerations.

What health services are covered by NY Community Medicaid?

Medicaid covers a variety of services depending on eligibility criteria, including:

- All regular medical checkups and required follow-up care,

- Immunization,

- Doctor and clinic visits,

- Medicine,

- Medical supplies, equipment, and appliances (e.g. wheelchair),

- Emergency care,

- Hospitalizations,

- Transportation to and from medical appointments,

- Transportation to and from hospitals,

- Nursing home care,

- Dental care.

While this is certainly not an exhaustive list, it should give you some idea of the medical services that Medicaid covers. A Medicaid planning attorney will help you gain a better understanding of your eligibility status and what covered services it entails.

How can I protect my house from Medicaid lien in New York?

You do not need to give away or sell your home if it is your primary residence to qualify for Medicaid in NY as it is considered exempt property. If you have a primary residence that is appraised for less than $955,000 you can qualify for community Medicaid, which in turn will allow you to receive home care aid hours. However, passing your house to beneficiaries after death can be tricky as Medicaid can ask for Medicaid reimbursement when a valuable asset is transferred through probate or administration. Thus, to protect your house from Medicaid liens and to make sure your beneficiary receives all assets outright and does not need to be stuck in probate or administration indefinitely, a Medicaid Asset Protection trust should be created by a reputable New York Asset protection and Medicaid planning lawyer.

Can I own a home and be on Medicaid in New York?

To qualify for Medicaid in New York, one must be below the state’s asset limit which is currently $30,182 for individual applicants and $40,821 for couples. An applicant's home is exempt from Medicaid eligibility considerations so long as it is their primary residence or, in the event they need nursing home care, they intend to return to it upon recovery. In these cases, the home equity interest, or the current value of the home minus any outstanding mortgage, must not exceed $955,000 for a Community Medicaid applicant and $1,033,000 for applicants seeking nursing home care (Nursing Home Medicaid). It must be noted that secondary or vacation homes are not exempt from Medicaid considerations.

If my spouse is going to a nursing home, can he transfer our home to me and qualify for Medicaid?

No, it is considered a marital asset. You will have to create an Irrevocable Trust and transfer your house into such a trust 5 years ahead of any Medicaid application for the transfer to be accepted by the nursing home. It is also in your spouse’s best interest to gift other financial assets that may help him or her qualify for Medicaid.

How long will it take for my NY Medicaid application to be accepted or denied?

In most cases, a decision will be made and provided to you within 45 days from the date you submit your application. However, if you are pregnant, applying on behalf of your children, or have a disability, the amount of time may vary.

What happens if my income exceeds the limit for NY Medicaid?

There are several options available to you if your income exceeds the limit for Medicaid:

- If you are applying for long-term Medicaid coverage and your spouse is not, you can transfer some or all of your monthly income to them as a community spouse via the Minimum Monthly Maintenance Needs Allowance (MMMNA), which they can use to cover living expenses.

- Applicants over the limit and applying for long-term Medicaid coverage can use the Medically Needy Pathway to subtract certain medical expenses from their monthly income. If after this deduction the applicant is below the Medically Needy Income Limit, which varies by state, they can qualify for long-term Medicaid coverage.

- Applicants can place excess income into a Qualified Income Trust.

- Applicants can explore a variety of revocable and irrevocable trusts that will allow them to relinquish official ownership of certain assets. This option must be done well in advance of any Medicaid application.

All these options should be explored with a Medicaid planning attorney to ensure that you qualify for the Medicaid coverage you need and your assets are protected.

Should I plan in advance?

Yes, it is recommended to plan well ahead of time. Unexpected circumstances may arise at any time and may prolong or complicate the planning process. Even if you or your family individual are not currently in need of Medicaid, it is better to be prepared instead of having to pay large out-of-pocket fees unexpectedly. It is recommended that you enlist the services of a skilled Medicaid planning attorney to handle your Medicaid planning.

How can my family and I be protected from long-term care expenses?

Medicaid planning involves creating a strategy to conveniently preserve your assets. Different clients may have differing assets and financial resources. Common tools used to protect assets and increase the likelihood of eligibility for Medicaid include: creating irrevocable trusts, life estates, and converting assets to non-countable assets.

Will Medicaid Pay for Nursing Home Care?

Yes, one of the benefits of receiving Medicaid is that it will cover the cost of nursing home care. If you are eligible and are planning on being admitted to a nursing home, Medicaid pays for the full care. However, it is essential to follow all the guidelines when receiving Medicaid to ensure that you avoid the risk of having it taken away, which will leave you in significant debt.

How much money can you have in the bank to qualify for Medicaid in New York?

Those applying for long-term Medicaid coverage can generally have up to $2,000 in their bank account(s). Every dollar after that will be counted toward Medicaid eligibility considerations. Those without further exemptions might find it difficult to qualify for all the services they need, though consulting with a Medicaid planning attorney will assure the best possible outcome for you and your family.

Can you own a car on Medicaid in New York?

A Medicaid applicant can own a car and not have it count toward their Medicaid eligibility under certain exemptions:

- They need the car for work.

- They need the car for transportation to medical appointments.

- They need their car for transportation in a rural area.

- Their car has been modified to accommodate a disabled person.

Any car a Medicaid applicant owns beyond the one qualified under one or more of these exemptions and is not otherwise their primary mode of transportation cannot exceed a value of $4,500; otherwise, it is considered part of their estate and will count toward liquid asset limits.

Will my Medicaid renew automatically?

With the end of the COVID-19 Public Health Emergency, the pause on yearly Medicaid renewal was lifted as of April 1st, 2023. Your Medicaid application will need to be renewed yearly and all pertinent information updated as necessary.

How many years does Medicaid look back in New York?

New York State’s Medicaid lookback law requires a lookback period of 60 months for those seeking long-term care Medicaid services. All gifts and asset transfers an applicant makes in the lookback period before their application date are subject to review and Medicaid eligibility requirements.

New York Community Medicaid will be implementing a Look-Back Period. The Look-Back period will be 30 months instead of the 60 months required for Long-Term Care Medicaid sometime in 2025.

What is Medicaid crisis planning?

Medicaid crisis planning is the urgent process of arranging finances and legal documents to help someone qualify for Medicaid quickly, usually because they need long-term care immediately. This often involves using legal tools such as asset protection trusts, transferring or spending down assets, and carefully preparing the Medicaid application to avoid penalties or delays. Crisis planning is especially important when a person is unexpectedly admitted to a nursing home or requires immediate at home assistance.

What is the Difference between New York Nursing Home Medicaid and Medicare?

Recent Cases Closed

Case 1:

A couple in their 70s came to us after one spouse was diagnosed with Alzheimer’s disease and required nursing home care. Their primary concern was preserving their home and life savings for their children while navigating Medicaid’s complex eligibility rules. New York Medicaid Planning Attorney Inna Fershteyn, implemented a multi-step legal strategy. First, she transferred their home and a portion of their savings into an irrevocable Medicaid asset protection trust, shielding these assets. For the “community spouse,” she utilized spousal impoverishment rules to allow retention of a higher portion of assets. Then she converted remaining liquid funds into a Medicaid compliant annuity, which transformed countable assets into an income stream exempt under Medicaid guidelines. Excess funds were legally spent down through necessary medical expenses. With thorough documentation and guidance throughout the application process, the client was approved for Medicaid within several months, allowing for significant cost savings and long term asset preservation.

Case 2:

A middle aged individual diagnosed with early onset Alzheimer’s disease was concerned about future long term care expenses jeopardizing their estate. Acting proactively, New York Medicaid Attorney Inna Ferhsteyn created a properly structured irrevocable trust to hold a substantial portion of their assets. We also assisted in the purchase of a Medicaid compliant annuity, converting the client’s remaining liquid assets into a non-countable income stream. These legal tools were carefully timed and executed to comply with all Medicaid transfer and income rules. As a result, the client secured Medicaid eligibility when the time came for care, while ensuring their estate would remain intact for their heirs.

Case 3:

A single woman in her 80s was unexpectedly admitted to a nursing facility after a sudden health decline, without prior Medicaid planning in place. Facing immediate nursing home costs totaling tens of thousands of dollars per month, her family sought urgent assistance. We performed crisis Medicaid planning, quickly transferring assets to an adult child caregiver. We also executed a personal services contract between the client and her daughter to compensate her daughter for years of unpaid care, legally reducing countable assets. Simultaneously, we spent down remaining funds on pre-approved expenses, including burial arrangements and final bills. With these measures in place, we submitted the Medicaid application promptly and achieved approval in under three months, saving the family hundreds of thousands of dollars in long term care costs.

Medicaid Planning Articles

What are the recent changes to Medicaid Eligibility in New York?

What is the Process of Applying For New York Medicaid in 2023?

Who Pays For Nursing Home If I Overstay The 90 Days?

Medicaid Eligibility After October 1st and New Look Back Provisions

Elder Law: The Medicaid application is a tough process

How Will Gifting Affect My Eligibility For Medicaid?

Testimonials

“The Law Office of Inna Fershteyn is truly exceptional! My grandparents worked with this firm for their estate planning and Medicaid needs, and they couldn't stop raving about the professionalism, expertise, and compassion they experienced. They were so impressed that they encouraged me to intern here and I couldn’t be more grateful for the opportunity! As an intern, I’ve seen firsthand the dedication the entire team has to providing top notch service to every client. Whether it’s guiding families through complex legal processes or crafting personalized solutions, the commitment to excellence is clear in everything they do. It’s inspiring to be part of a team that truly makes a difference in people’s lives. If you’re looking for a law office that combines knowledge, care, and results, I can’t recommend the Law Office of Inna Fershteyn enough!” – Anna

“I live in VA and am the POA for my aunt in NY. I needed information regarding Medicaid, finances, etc. I found Inna online and she had amazing written reviews, so I made an appointment. I just finished our Zoom, and she was SO pleasant and caring. She took her time and didn’t rush the call. She gave me sound advice that actually took herself out of the equation and saved us money. I know who I’ll be calling for any future issues. The consultation fee was reasonable and worth it as it saved us a lot more than the fee. I highly recommend Inna for her empathy alone. OH! Did I mention she’s really professional and knowledgeable too. She loves what she does. – Ayanna F.

“I highly recommend Inna Fershteyn for help with trust and estate planning and elder law. She is great at explaining things in a way that’s easy to understand, especially when it comes to planning for the future and navigating Medicaid rules. If you need someone compassionate and knowledgeable, Law Office of Inna Fershteyn and Associates, P.C. is the one to go to.” –Alexandra T.

“I can't recommend the Law Office of Inna Fershteyn highly enough for estate planning and Medicaid planning for the elderly. We had an emergency situation where an irrevocable trust had to be set up and Medicaid had to be obtained right away and Inna and her team prepared all the documents for my relatives in less than one week. Inna is truly the best elder care lawyer in NY.” -Luis B

“Even after the Medicaid Planning was done, Inna was always available to answer more questions and guide us through additional steps of the process. Our family loved the office and would recommend the Law Office of Inna Fershteyn to anyone who is looking to do their Medicaid or Estate Planning.” – Jessica G.

“Inna was very courteous, understanding and most importantly experienced. I ended up doing a Revocable Living Trust, Will, Living Will and Power of Attorney and later on I came back to Inna to do my Medicaid Planning.” – Natalia B.

New York Medicaid Planning Resources

Medicaid - General Information:

Medicaid Consumer Enrollment & Coverage:

- Dual Eligibility

- Early and Periodic Screening, Diagnostic, and Treatment Services

- Medicaid Dental Coverage

- Medicaid Eligibility

- Mental Health Services

- Third Party Liability

New York Resources